How does a Roth IRA work?

Let’s explore the intricacies of the Roth IRA.

Definition

The Roth IRA is an Individual Retirement Account that you can contribute money to every single year for retirement.

- Money Restriction: As of 2022, those under the age of

50can contribute up to$6,000per year and those 50 and above can contribute up to an extra$1,000per year. - Age Restriction: Once the money is put into this account, you cannot withdraw it until you are

59.5years old. Unlike 401k and like HSAs, you are not forced to take distributions (withdrawals) when you turn70.5years old (Required Minimum Distributions). - Penalty: There are many withdrawal rules for the Roth IRA as we’ll see below.

- Tax-Advantage: The Roth IRA is what is known as a tax-advantaged account.

Withdrawal rules

The IRS really only cares about two things:

- The

5-year rule: if you’ve had five tax years after your first Roth IRA contribution - If you’re under

59.5years old

Here are the withdrawal rules:

- You can always withdraw the amount you contribute from a Roth IRA (almost like an emergency fund)

- If you’re under

59.5, the money will be taxed as income and penalized 10%- You can avoid the penalty if the money is used for a first-time home purchase, if you’re permanently disabled, or if a beneficiary takes the distribution

- You can also avoid the income tax if you meet the

5-year rule

- If you’re over

59.5, you will not be penalized for any withdrawals- You can avoid the income tax if you meet the

5-year rule

- You can avoid the income tax if you meet the

In any other situation, if you withdraw funds, that money will be taxed as ordinary income and the IRS will impose a 10% penalty.

Tax-advantaged account

There are 3 ways you can obtain tax benefits in any investment account:

- When you put money in

- When your money grows

- When you take money out

The Roth IRA takes advantage of numbers 2 and 3.

- Taxed Contributions: the money you place in your account is already taxed (post-tax money)

- Tax-Free Growth: gains from growth, dividend payouts, and accumulated interest are not taxed

- Tax-Free Withdrawals: distributions, or funds you withdraw, are not taxed

Key Points

- The Roth IRA is a Roth Individual Retirement Account

- We can only withdraw money after

59.5(within the rules) - We can withdraw whatever we put in

- Those under the age of

50can contribute$6,000/yr - Those

50and over can contribute an extra$1,000/yr - Tax-free growth and withdrawals

Eligibility

In order to be eligible for a Roth IRA, you simply need earned, taxable income (but not too much).

As of 2022, singles making an income of $129,000 per year and families making $204,000 per year cannot contribute to a Roth IRA.

The more popular options to start investing in a Roth IRA include Fidelity, Vanguard, Charles Schwab, or M1 Finance.

Other Things To Know

1. Don’t Miss Out on the Tax Savings

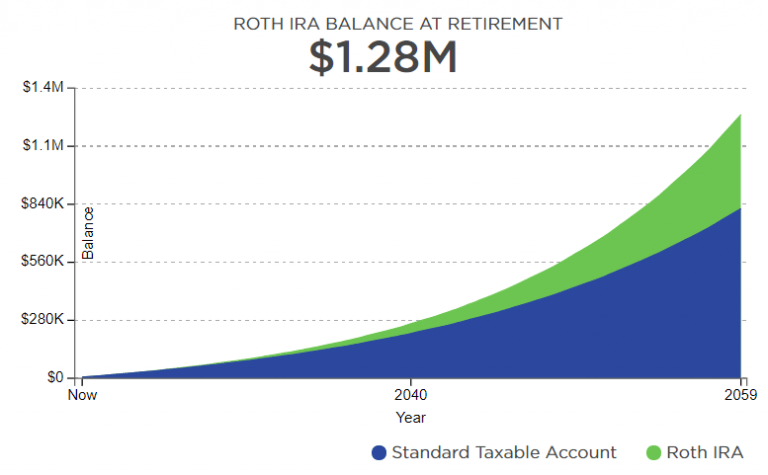

Let’s say I started maxing out my Roth IRA at $6,000 every year.

After 40 years, I would have $1,280,000 in my Roth IRA if I invested it in the S&P 500 (average 7% annual return).

If I invested that same money into a taxable brokerage account, I would have $822,000 in that account.

I saved ~$457,000 in taxes. That is mind-blowing. That is also why you should start investing in a Roth IRA today.

2. High-Income Earners Are Not Hopeless

You’re not out of luck if you make a lot of money.

Be sure to read up on Backdoor Roth IRAs in order to maneuver your way around the income limits.

3. Diversify Your Assets

When people think of diversification, they often think about investing in different funds, which is important.

You never want to put all your eggs in one basket. Don’t use all your money to buy a single stock, but perhaps buy index funds that track the entire market or follow the three-fund portfolio.

That being said, having a Roth IRA be your only investment means that if you retire when the stock market is down, then you gotta wait years for it to get back up, delaying your retirement.

Be sure to diversify your assets (e.g. real estate, savings accounts, CDs, cash, Roth IRA, etc.)

Conclusion

The Roth IRA is available to most of us in the USA. It’s a great investment account and will let you grow your money in the long run.

Just make sure you understand what you’re investing in, and continue to spread out your investments so that you’re all set for the future.