How To Open a Fidelity Roth IRA: A Step-by-Step Guide

Coming to the realization that we need to start saving for our retirement is the most important first step to take in securing our financial future.

We see the terms Roth IRA, 401k, and HSA thrown around, and we don’t understand what any of it means until we watch a Graham Stephen video or read Investopedia.

There are plenty of resources online to help us understand the inner workings of Roth IRAs. I would recommend we all take some time to sit down and read about how IRAs differ from other retirement accounts before diving into anything.

Let’s check out a brief overview of the Roth IRA.

Brief Roth IRA Overview

A Roth IRA is a retirement plan that offers tax-free growth and tax-free withdrawals in retirement.

You can place post-tax money into your Roth IRA, meaning that any money in your Roth IRA is going to come from your own bank account. You’ve already paid taxes on the money going into the account, and you can withdraw the money tax-free when you retire. It is often one of the first steps to saving and potentially retiring early.

The Roth IRA is a great option if your tax rate now will be lower than your tax rate in retirement. If you believe you will be in a higher tax bracket when you are in retirement, then you should start investing in a Roth IRA.

Tax rates differs depending on our income. Suppose I am single and am making $75,000 per year. I would have a tax rate of 22% as of 2022.

| Tax Rate | Single |

|---|---|

| 10% | $0 to $10,275 |

| 12% | $10,276 to $41,775 |

| 22% | $41,776 to $89,075 |

| 24% | $89,076 to $170,050 |

| 32% | $170,051 to $215,950 |

| 35% | $215,951 to $539,900 |

| 37% | $539,900 or more |

If I have any reason to believe my income will increase beyond the 22% threshold by the time I’m 59 1/2 years old, then I can take advantage of the Roth IRA. Even though I’ll be in a higher tax bracket, the money will not be taxed at all when I take it out at 59 1/2.

You can find a complete table of the tax rates.

Even if you don’t plan on working during retirement, it’s quite useful to take advantage of this tax-advantaged account.

That being said, there are limits to the Roth IRA. If you are single and make over $144,000 per year, then you are limited in your Roth IRA contributions. There are ways to circumvent this issue with a Backdoor Roth IRA.

If a Roth IRA is available to you, it’s best to start contributing as early as possible.

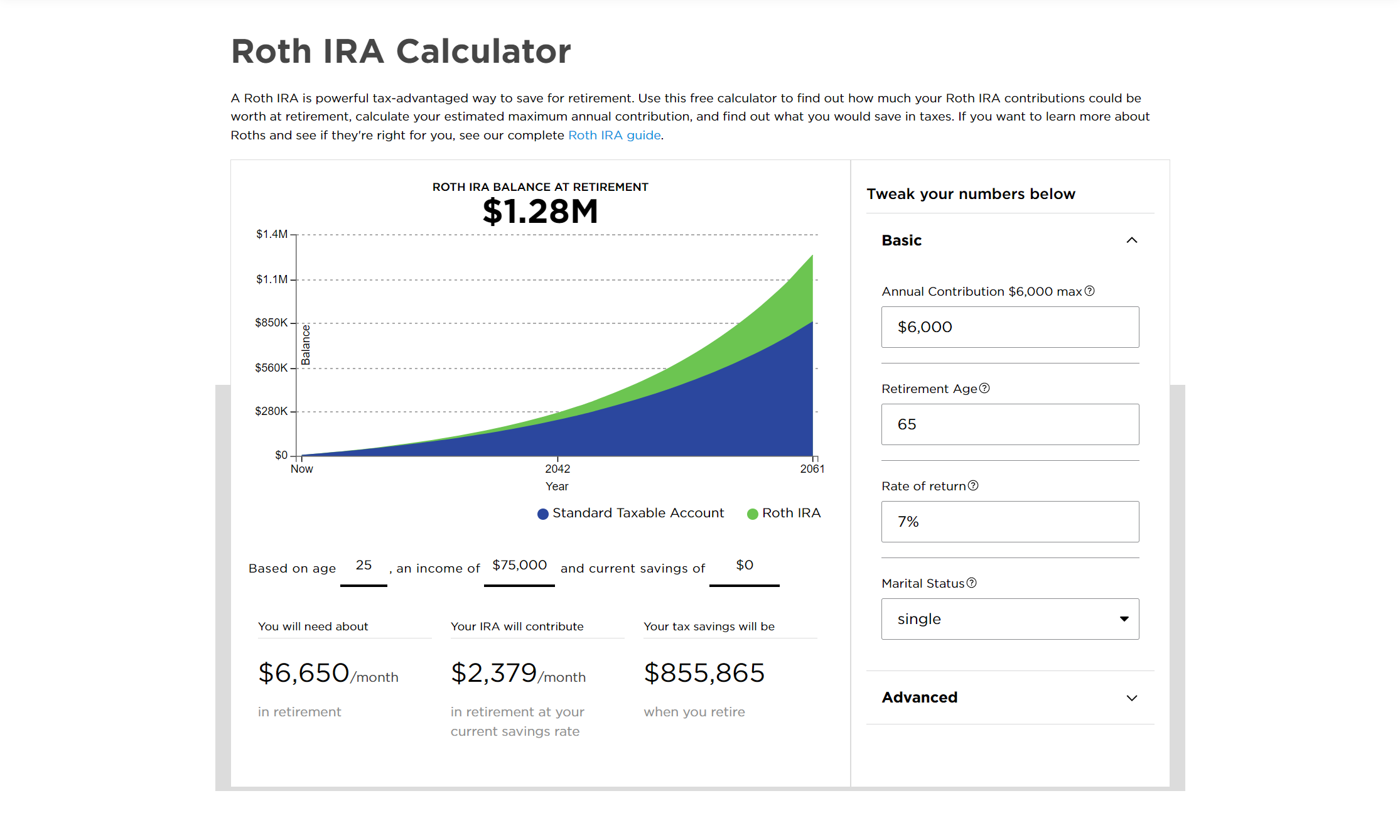

Check out this graph from NerdWallet’s Roth IRA Calculator.

If you were to invest $6,000 every year in the S&P 500 (average 7% rate of return) from the age of 25 to 65, you would have $1,280,000 in your Roth IRA and would have saved $424,000 in taxes.

The best part is that you would only have contributed $6,000 * 40 years = $240,000 of your own money into the account, making you $1,280,000 – $240,000 = $1,040,000.

How to Invest in a Roth IRA with Fidelity

I’ll walk you step-by-step through how to invest your first dollar into an index fund that tracks the S&P 500, which simply measures the stock performance of the United States' 500 largest companies.

This is a smart and simple way to start investing. Picking stocks that beat the market consistently is tough. With the S&P 500, if one stock fails, you have the other 499 stocks to keep you afloat. This index fund has averaged a 7% rate of return in its lifetime.

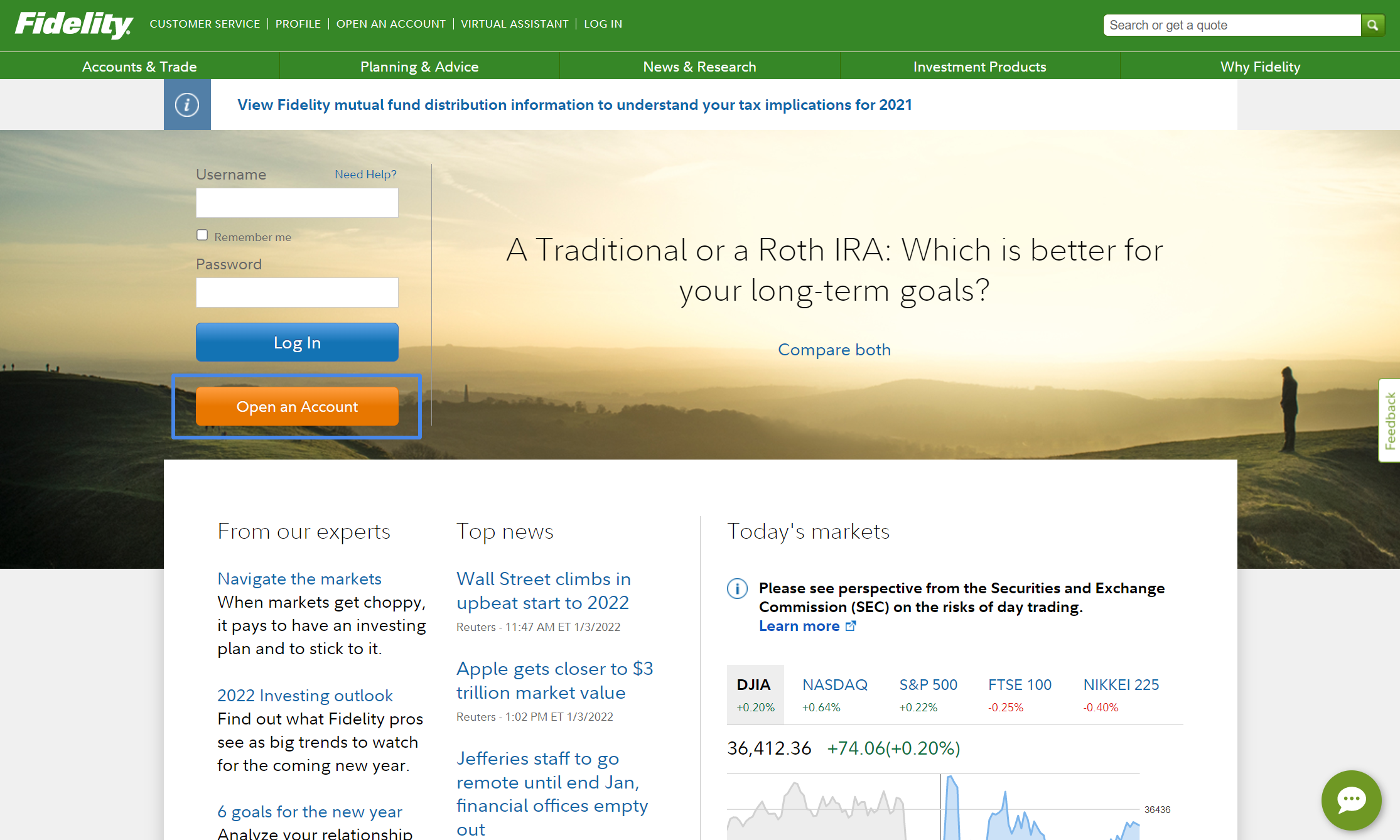

Step 1: Open a Fidelity Account (Roth IRA)

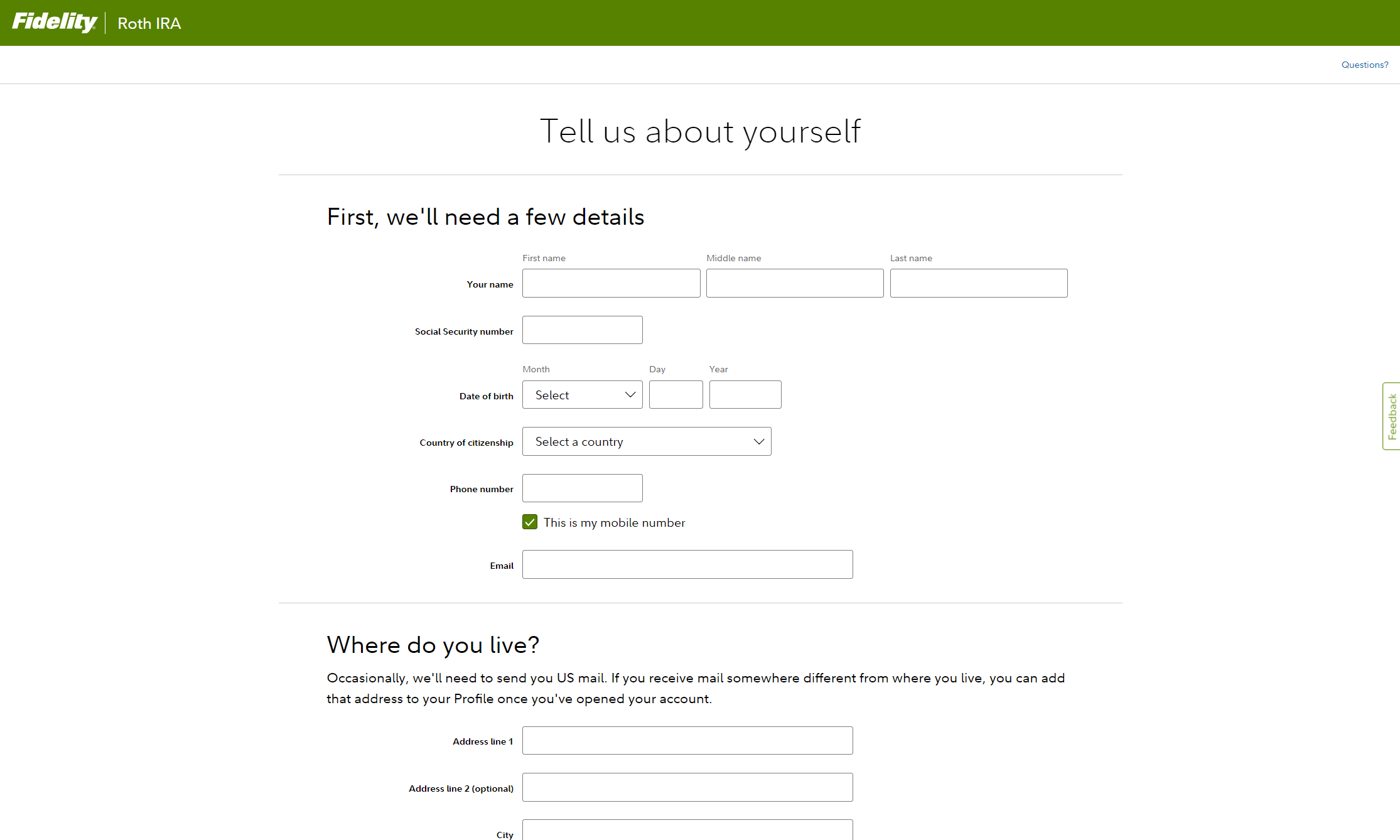

First, we want to register an account with Fidelity (you’ll need your name, SSN, DoB, etc).

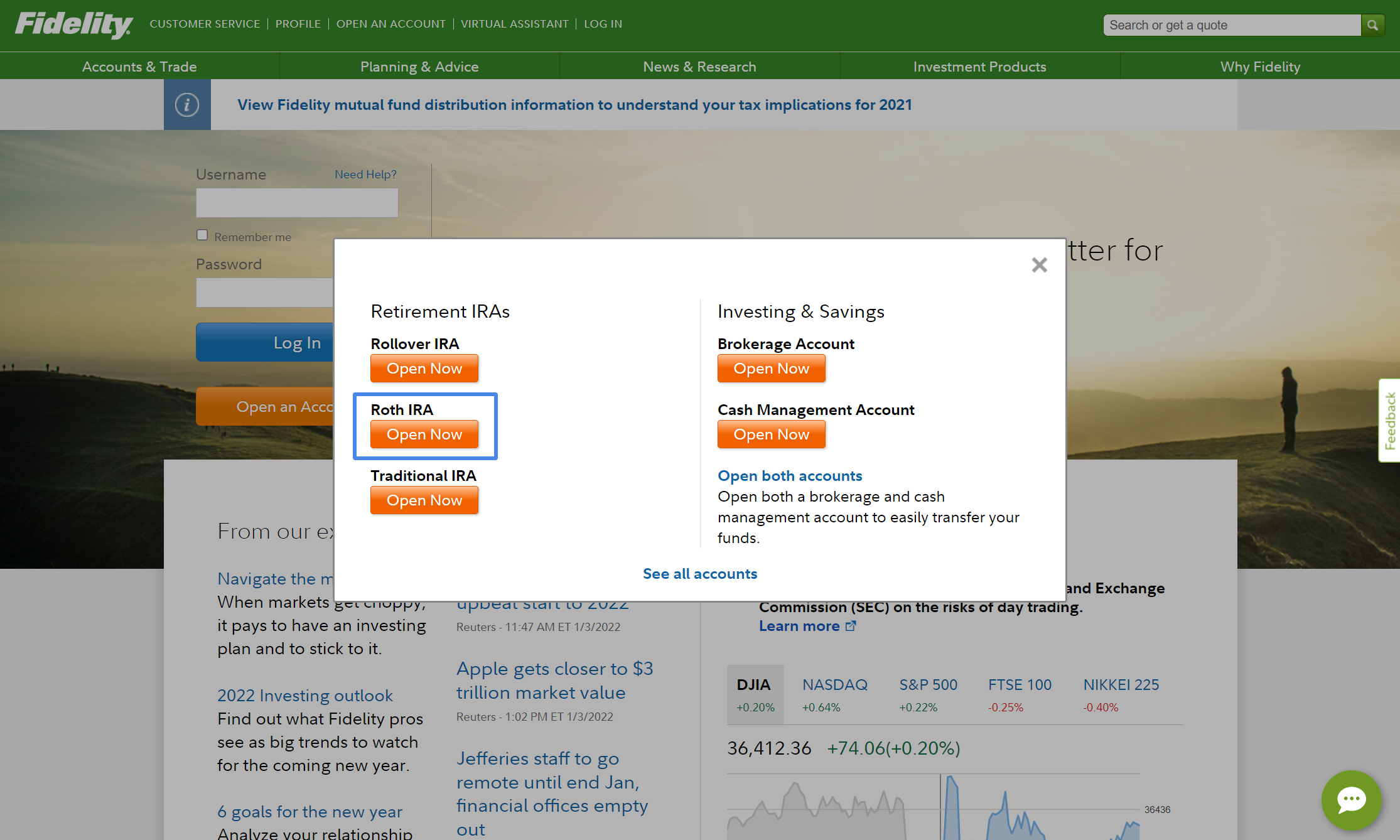

Select Open an Account.

Choose Open Now under Roth IRA.

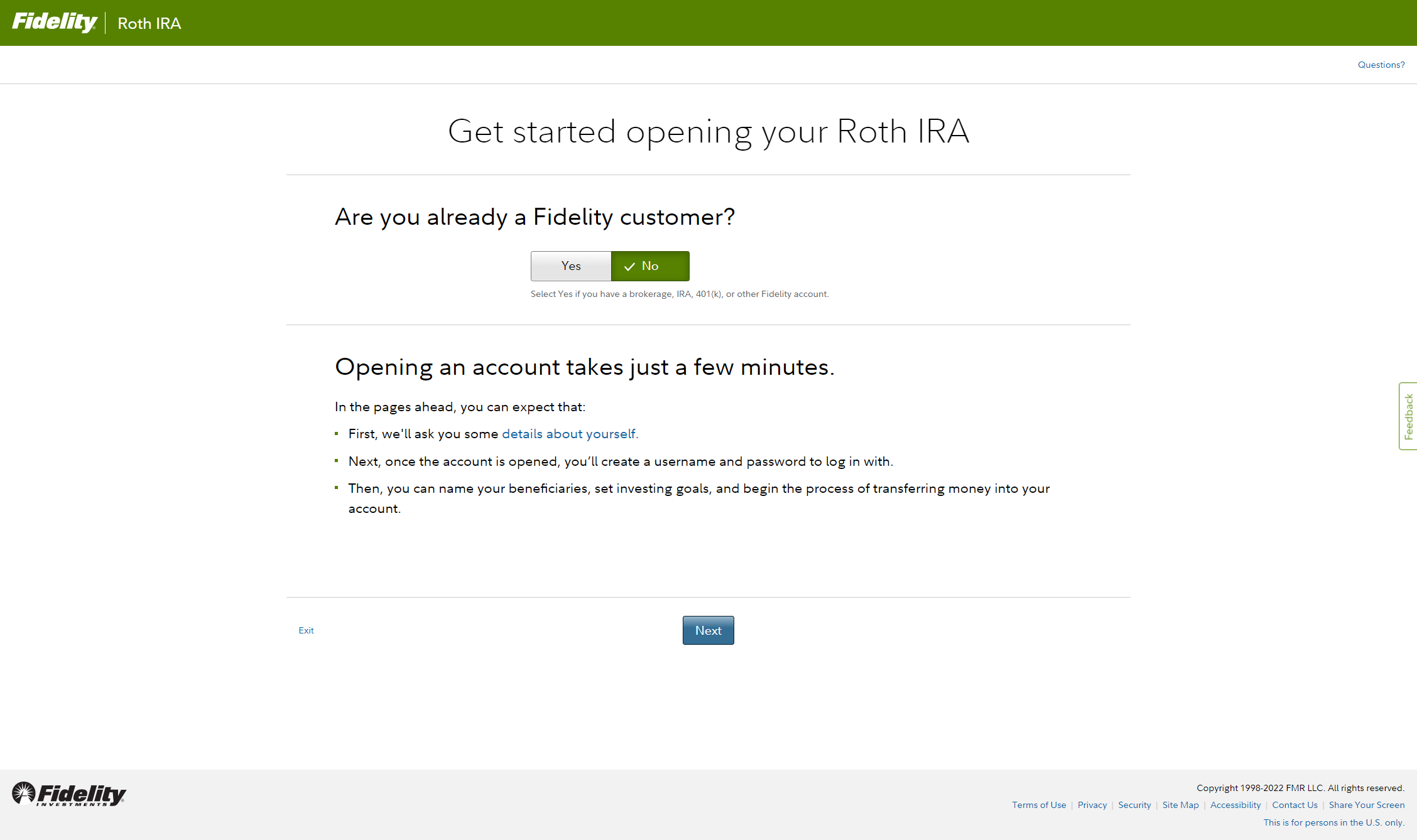

You’re probably not a customer yet if you’re reading this article 🙂

Enter your personal information here.

Employment Status. You may be asked about your Employment Status. This can be modified at any time, so don’t worry too much about the specifics.

Core Position. You may also need to select your Core Position. This is where your money resides when it’s not being invested. For the most part, it doesn’t matter which one you select. Your money should pretty much always be invested. All that being said, choose SPAXX.

Congratulations! You’ve successfully registered an account with Fidelity. Verify that you received a confirmation email upon registration.

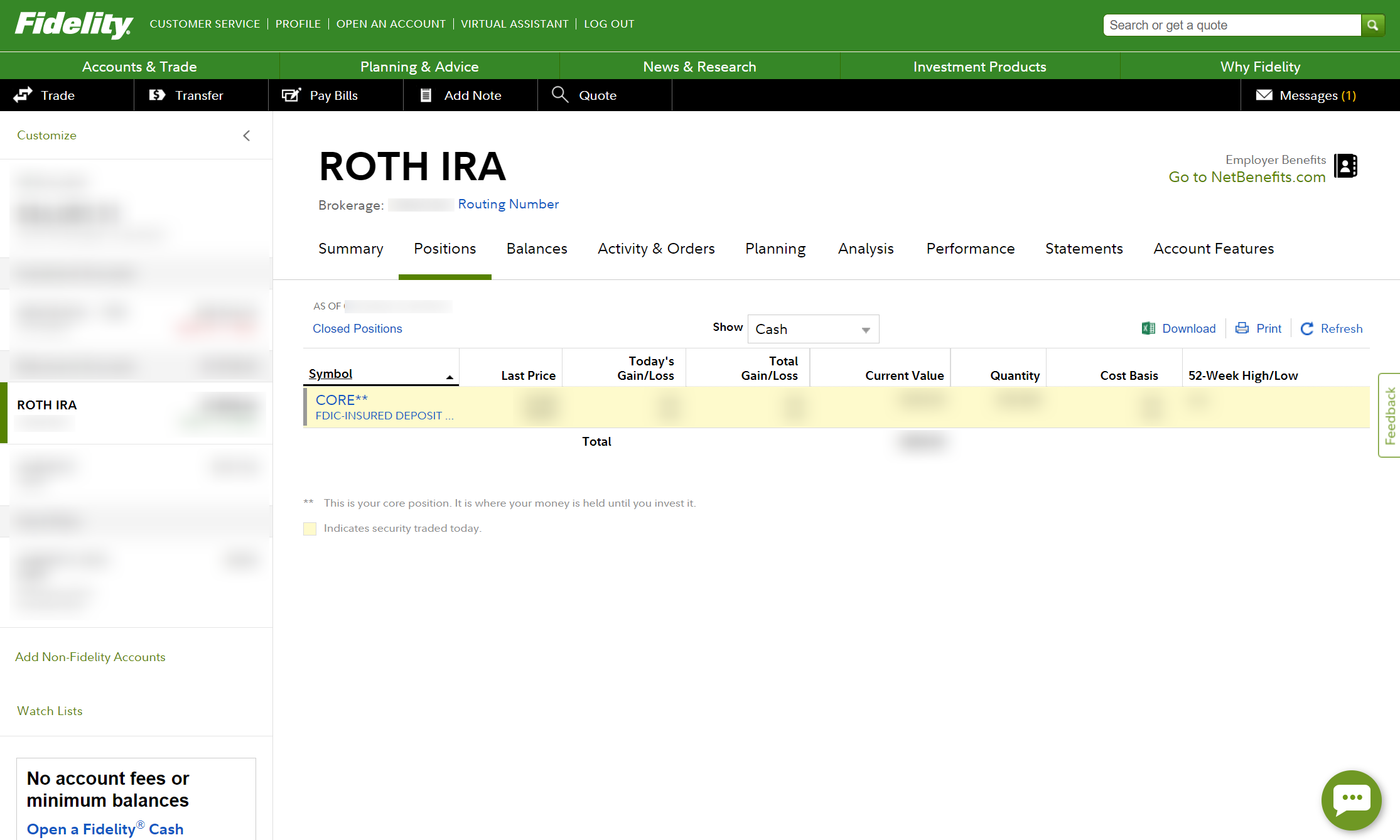

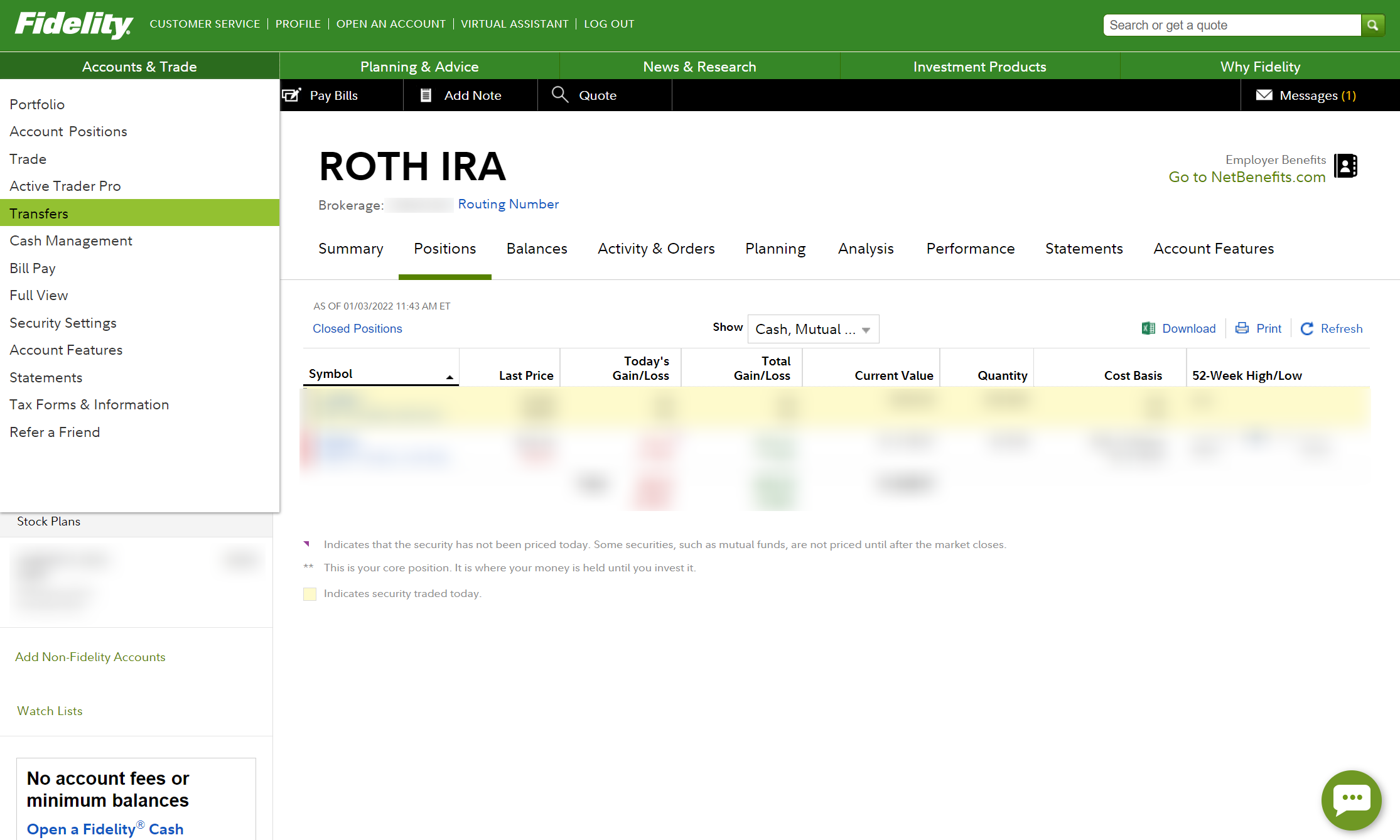

You should see a Dashboard when you log in. The Positions tab will tell you where your money is invested in all your investment accounts. Currently, you should have no investments.

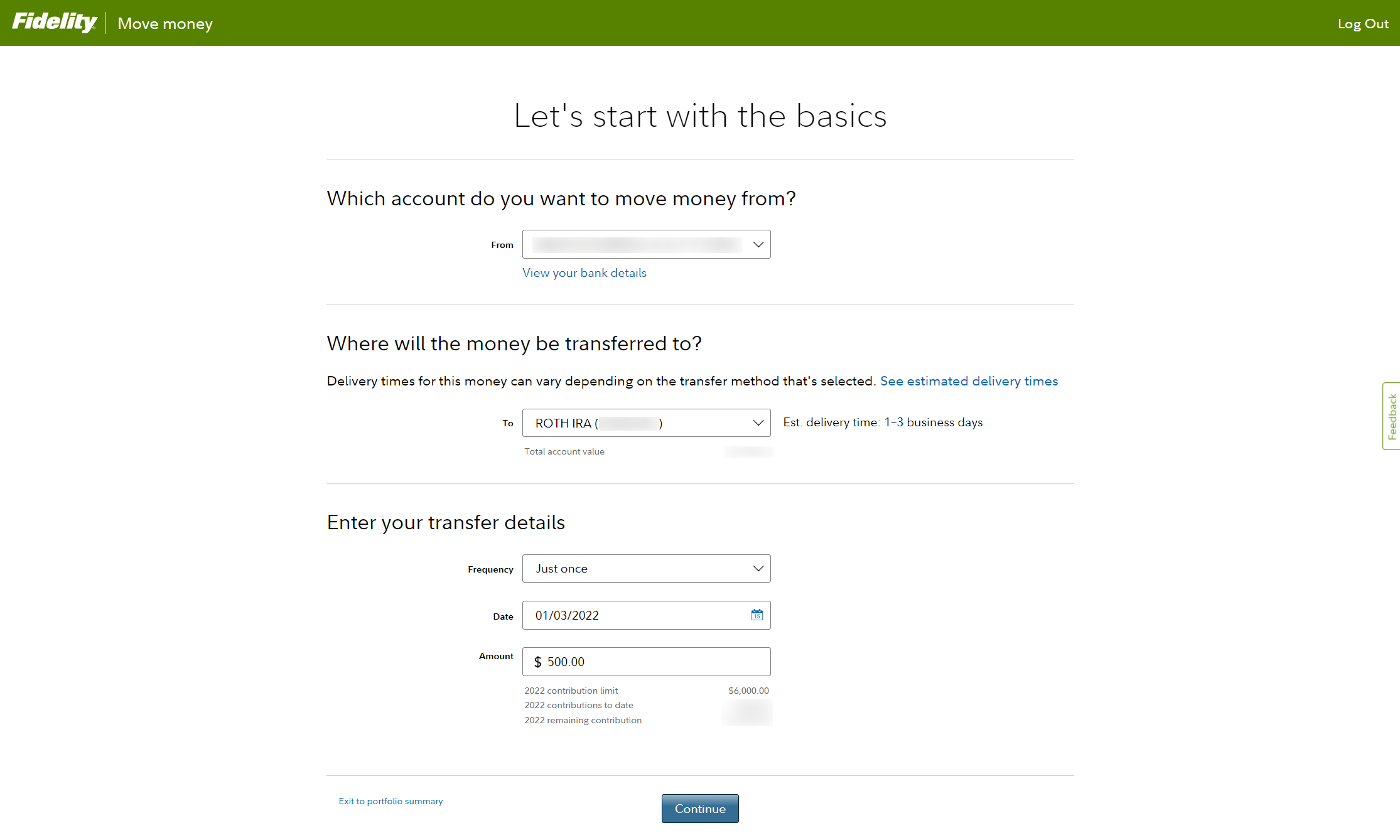

Step 2: Transfer Money Into Your Roth IRA

Next, we need to transfer money into the Roth IRA. Money transferred will go into the Core Position, meaning it’ll just sit in your account as if it’s sitting in your checking account. It’s not invested, yet, but you still need to take this step.

Select the Transfer tab.

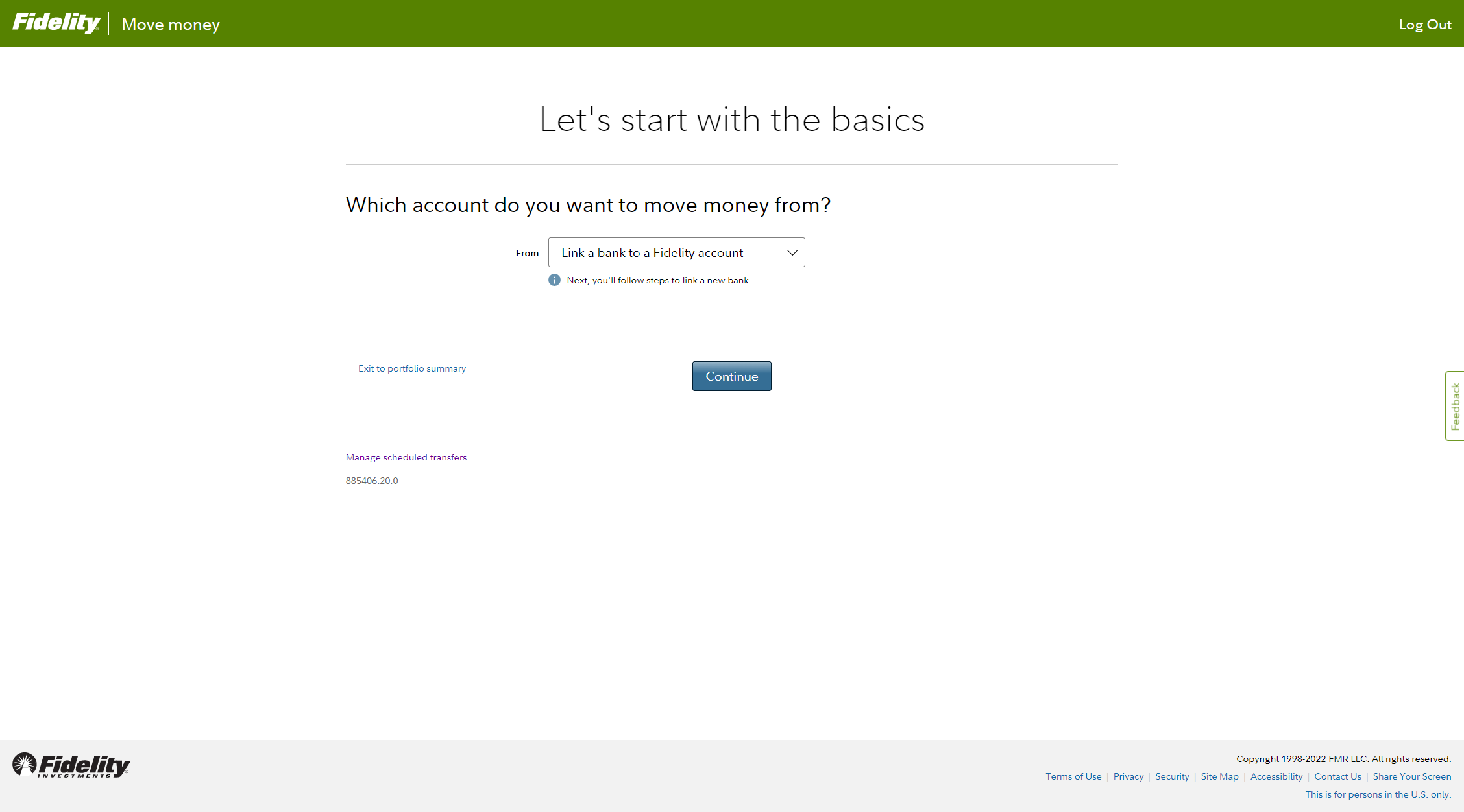

In the From section, select Link a bank to a Fidelity account and follow the instructions to add your bank account.

Then, you’ll want to set From to be your bank account and To to be your Roth IRA.

You may have the option to select your contribution year as well. You can contribute to the previous year until April of the current year. It’s always best to max out the previous year before getting started on this year so that you have more money to contribute in the future.

Select Continue.

Once you have confirmed the transfer, it will take approximately one business day until the transfer is complete. So, now you can take a break.

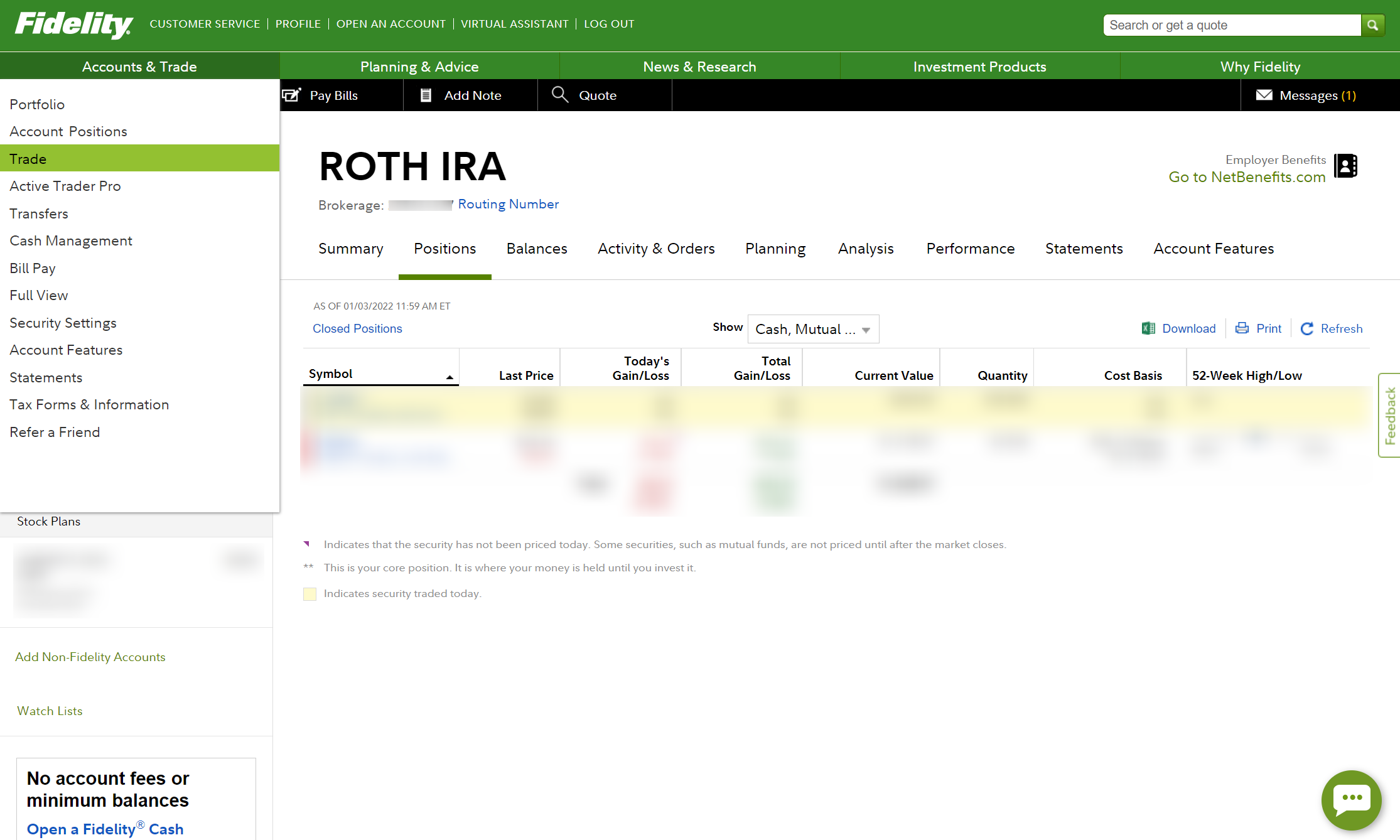

Step 3: Invest in Stocks Inside Your Roth IRA

Once you have the money transferred into your Roth IRA, the Core Position row should show the amount of money transferred.

This money is not invested, yet.

I repeat.

It is not invested.

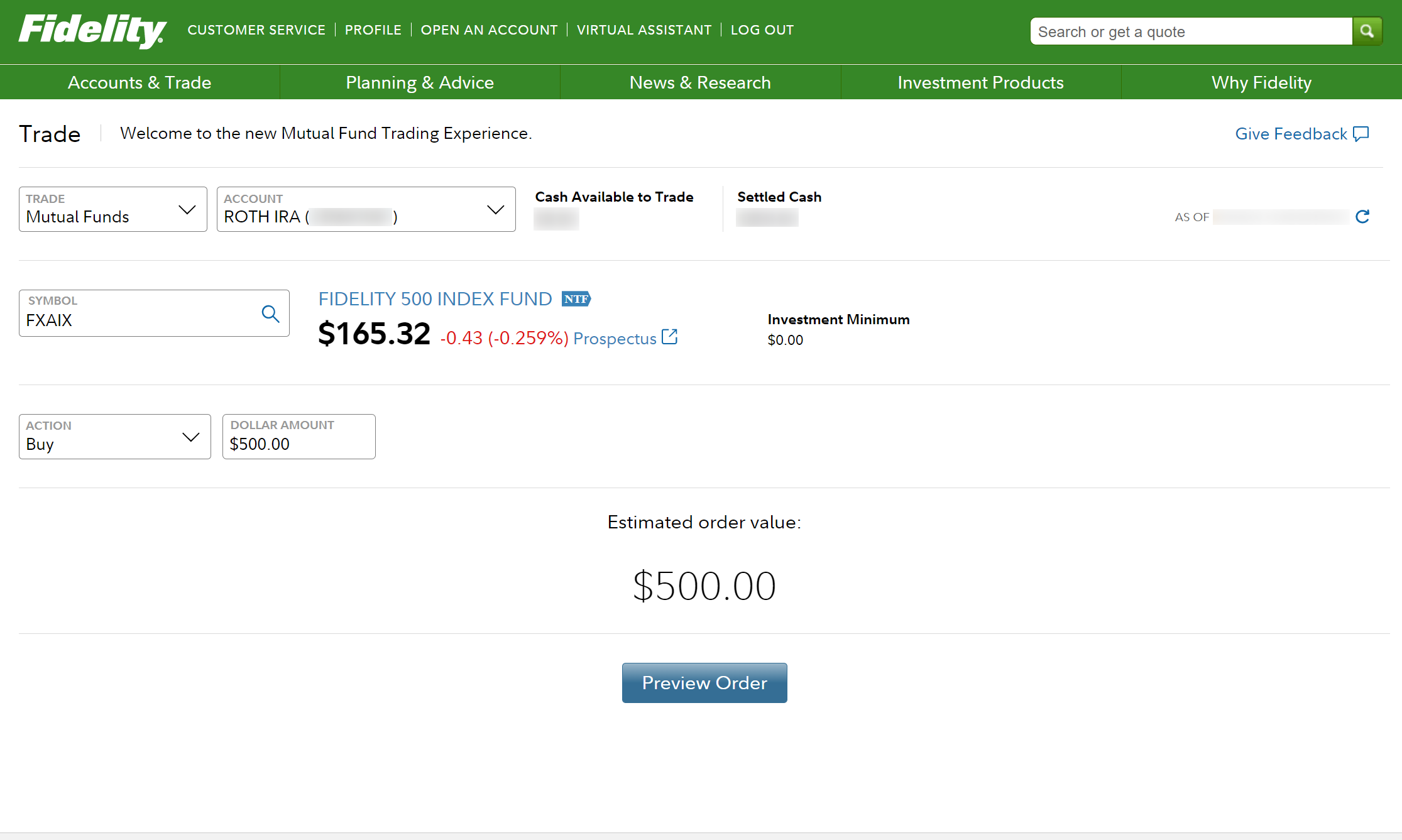

In this example, we will use the money transferred into our Roth IRA to buy

FXAIX, the Fidelity S&P 500 index fund.

First, select the Accounts & Trade tab, then select Trade.

Choose your Roth IRA as the account.

Choose Mutual Funds as the Transaction Type. Search FXAIX as the Symbol.

It should also say how much money you have available to buy these funds next to Cash Available to Trade.

Select Buy as the Action and input the amount of money you want to use to buy this index fund.

Select Preview Order and confirm the order.

Great! You’ve invested your first dollar.

Step 4: Set up Automatic Monthly Investments

Now that you’ve invested some of your money, it would be a great idea to make this a recurring payment. To max out your Roth IRA in 2023, you would ideally be investing $6,000 / 12 = $500 per month in your Roth IRA.

That is a lot of money for many people, so let’s make that our goal. Maybe you’ll want to start with $50 per month and then slowly work your way up there.

In this example, we’ll start automatic monthly investments into

FXAIX(S&P 500) every3rdof the month.

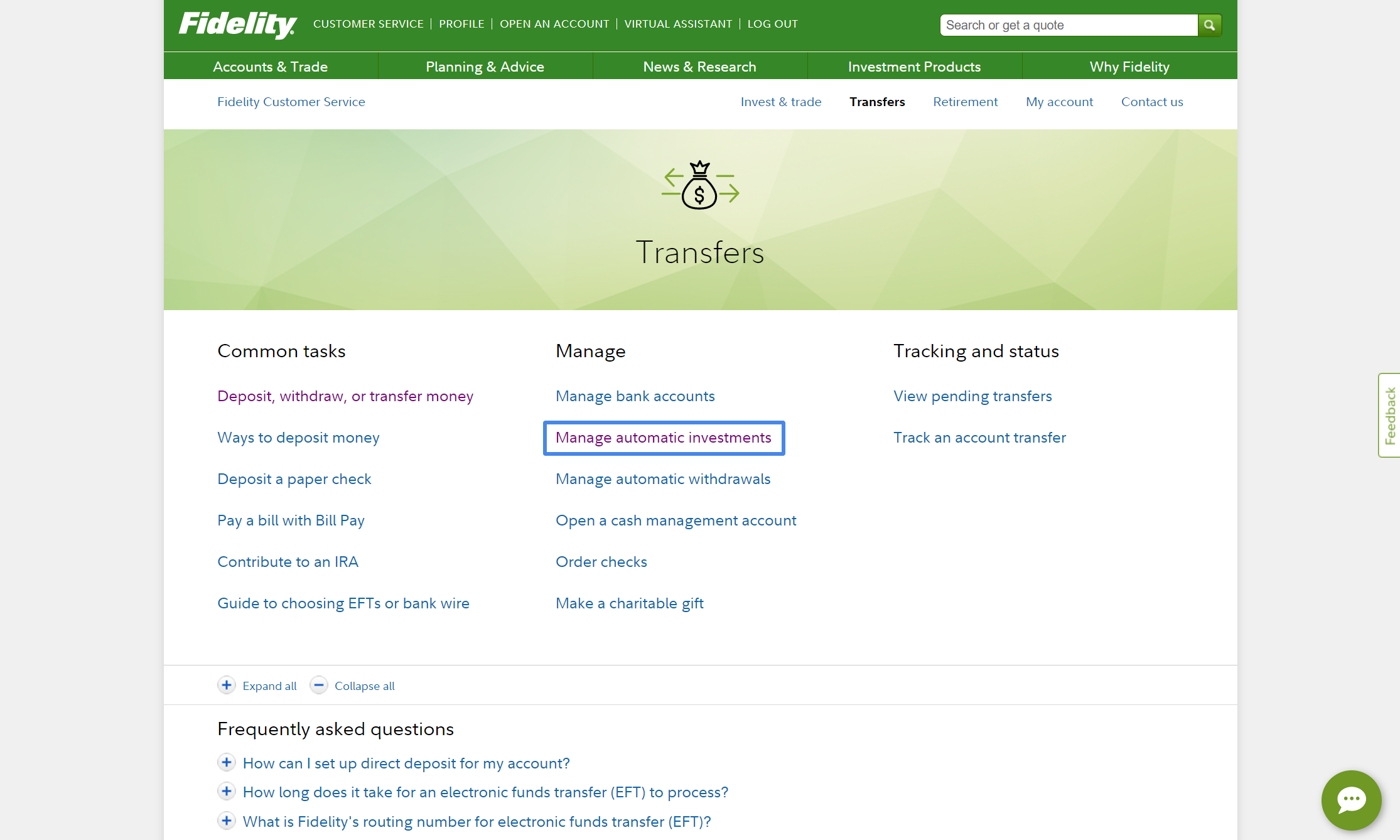

First, we’ll go to Accounts & Trade and select Transfers.

Select Manage automatic investments.

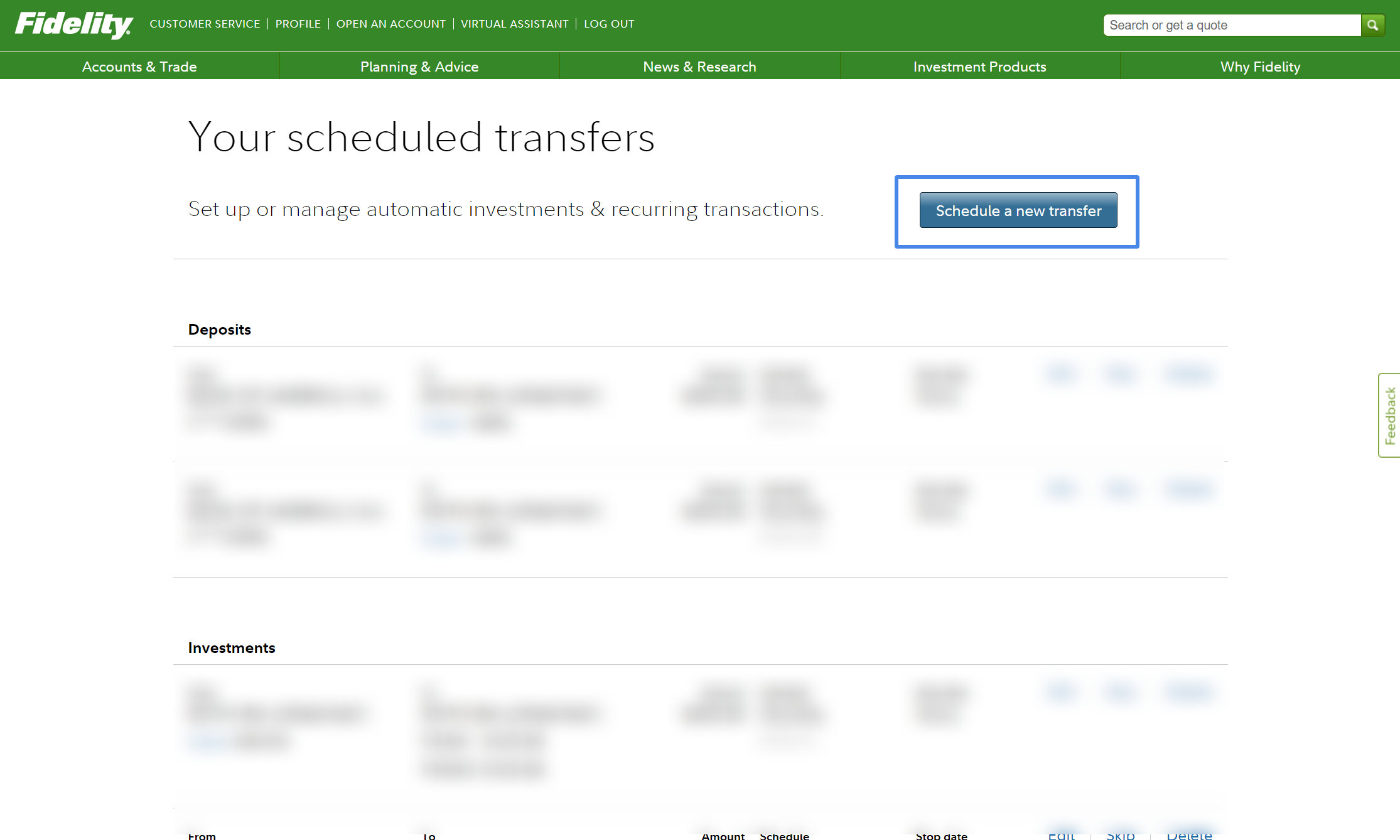

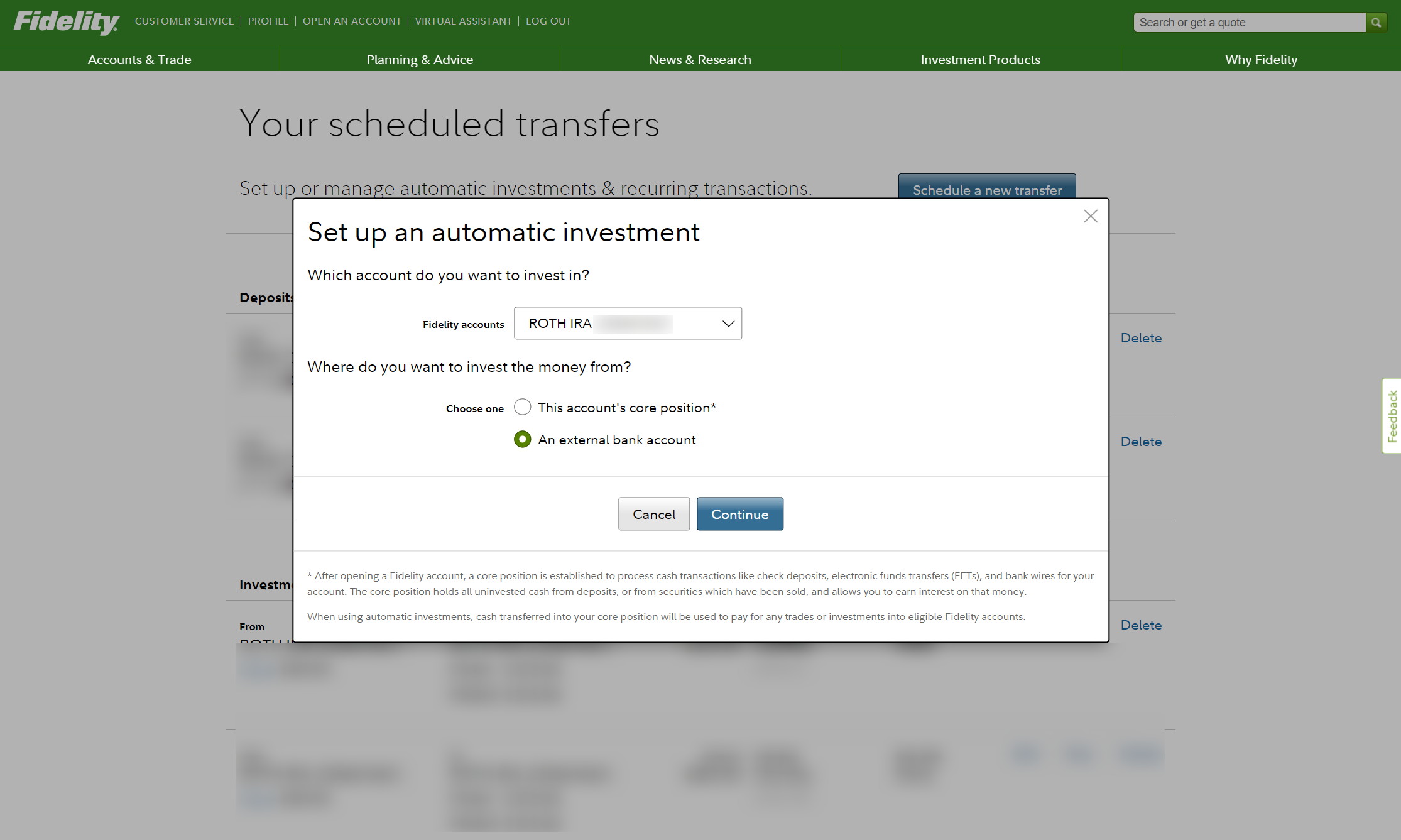

Select Schedule a new transfer.

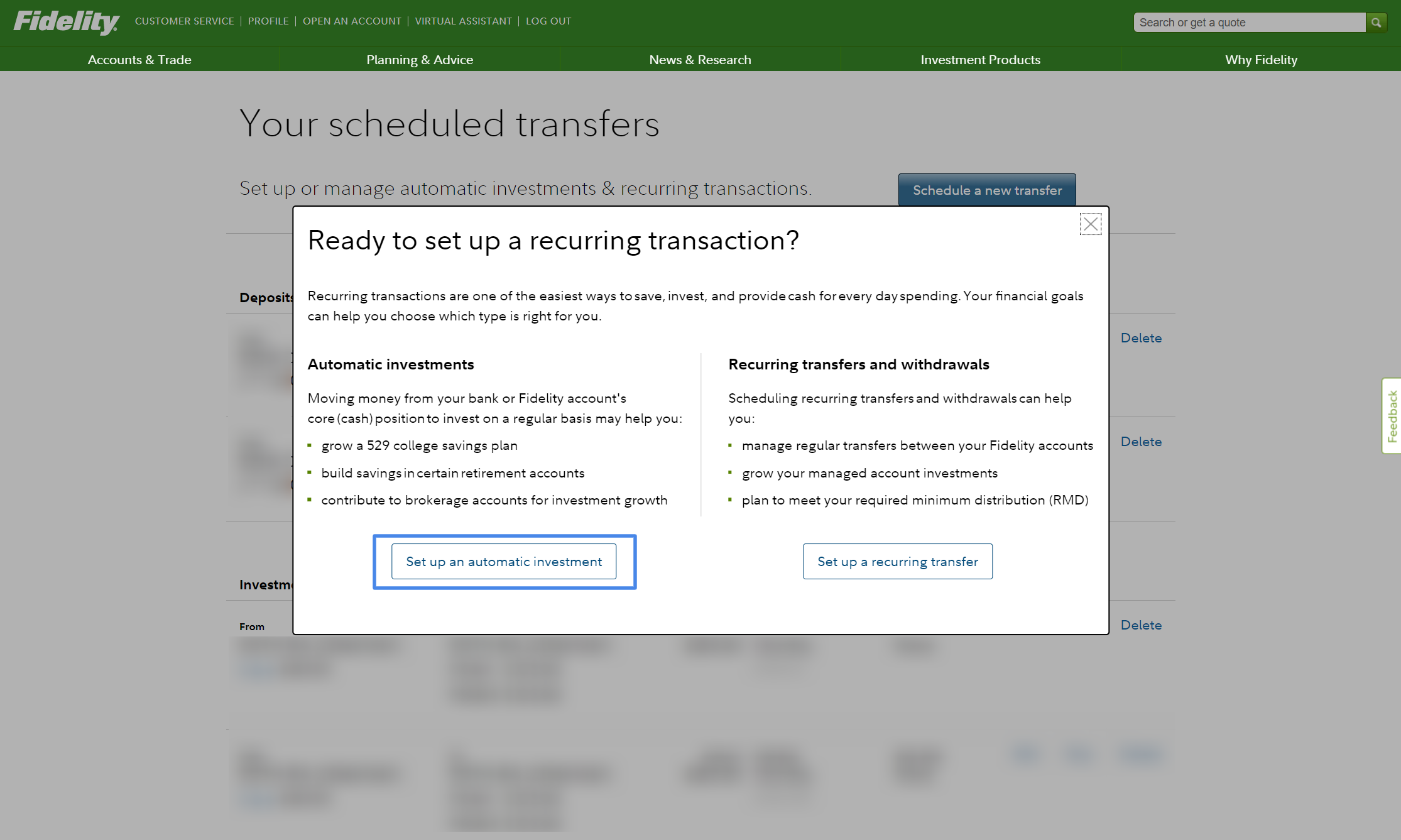

Select Set up an automatic investment.

We want to transfer funds from an external bank account into our Roth IRA.

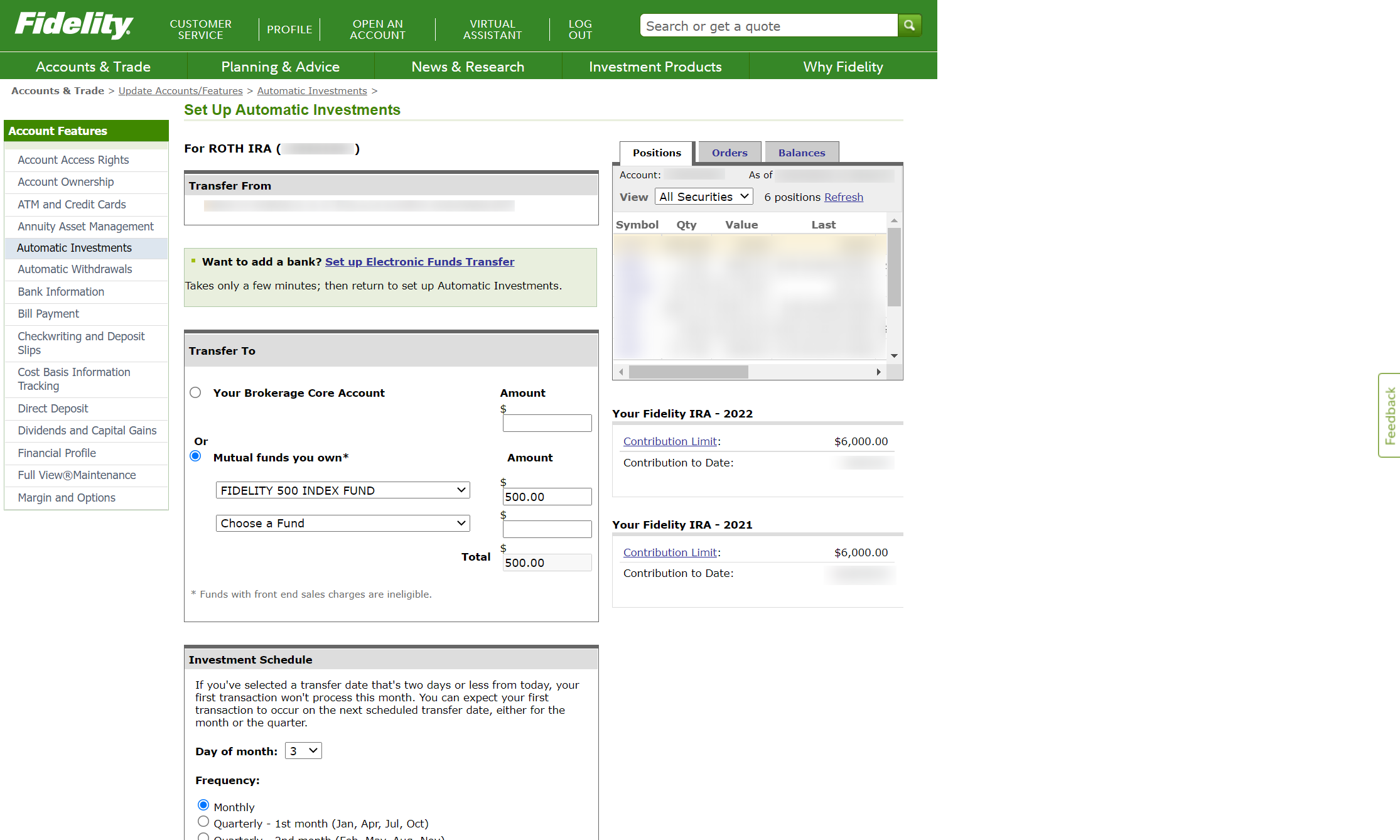

Within Transfer To, select Mutual funds you own.

If FIDELITY 500 INDEX FUND shows up, choose that option and enter the monthly amount to the right. If it doesn’t show up, wait until the next business day for your previous trade in Step 3 to complete. You can modify all of this at any time.

Finally, we’ve set up our automatic monthly investments in our Fidelity Roth IRA!

Conclusion

Congratulations! You’ve gone through the process of setting up your Roth IRA.

There are many different strategies that people use to determine their investments (e.g. target-date retirement funds, three-fund portfolios, etc.).

I’m a big fan of the “100% stock investments until I’m old” strategy, which includes the S&P 500 and small-cap stocks. That is something for you to research and decide on your own. I may write up an article on my asset allocation and motivation behind it.

Best of luck to you and your investing 🙂