How does a Health Savings Account (HSA) Work for Retirement?

Everyone’s talking about the 401k, the Roth IRA, and how you can invest in those accounts for retirement.

However, fewer people mention the HSA, or Health Savings Account, as a means to retirement.

Let’s explore how we can use the HSA for our own retirement.

Definition

An HSA is a savings and investment account that you can contribute to every single year.

- Money Restriction: As of 2022, single people can contribute up to

$3,650per year and families can contribute up to$7,300per year. Unlike Flexible Spending Accounts (FSA), your HSA funds do not expire annually, so your money will roll over into each subsequent year. - Reimbursable Expenses: Once the money is put into this account, you can only withdraw it for qualified medical expenses: acupuncture, flu shots, body scans, chiropractor, contact solutions, glasses, doctor’s appointments, surgery, therapy, wigs, X-rays, guide dogs, etc.

- Penalty: If you withdraw funds for any other purpose, that money will be taxed as ordinary income and the IRS will impose a

20%penalty. - Age Restriction: That being said, at

65years old, your HSA functions as a traditional IRA, meaning you can use your money for anything at that point. As with Roth IRAs, there is no Required Minimum Distribution (RMD), which is just the minimum amount you are required to withdraw from your account after you reach the age of70.5. - Tax-Advantage: One last feature of the HSA is: you get triple tax savings.

There are 3 ways you can obtain tax benefits in any investment account:

- When you put money in

- When your money grows

- When you take money out

The term “triple tax savings” takes advantage of all three tax benefits.

- Tax-Free Contributions: the money you place in your account is not taxed (pre-tax money)

- Tax-Free Growth: gains from growth, dividend payouts, and accumulated interest are not taxed

- Tax-Free Withdrawals: distributions, or funds you withdraw, are not taxed

Triple tax savings means an HSA is a

100%tax-free savings or investment account.

Key Points

- The HSA is a Health Savings Account

- We can only withdraw money for qualified medical expenses

- If we withdraw for an unqualified expense, we will pay income tax plus a

20%penalty

- If we withdraw for an unqualified expense, we will pay income tax plus a

- HSA will function as an IRA at

65years old - Single Contribution Limit:

$3,650/yr - Family Contribution Limit:

$7,300/yr - Triple tax savings

Eligibility

In order to be eligible for an HSA, you need to:

- Be over

18years of age - Not claimed as a dependent on someone else’s tax return

- Enrolled in a high-deductible health plan (HDHP), a plan with a higher deductible than a traditional insurance plan.

Deductibles refer to the amount you pay your health care before your insurance company begins to pay. A higher deductible means you pay for more of your initial health care costs, but you also pay lower monthly premiums. This amount depends on your insurance plan and what your insurance covers.

There are two ways to start investing in an HSA:

- Employer-sponsored: If you’ve chosen an HDHP, then you should be HSA eligible (they may even contribute to your HSA for you)

- Self-directed: As long as you’re enrolled in an HDHP, then you can choose your own HSA provider (e.g. Lively, HSA Bank, Health Equity)

Advantages of an HSA (the exciting part)

So, the HSA is just a tax-free account for medical expenses. True.

But here are 4 ways you can take advantage of your HSA.

1. You Can Invest Your Money

When you open an HSA, you have the option to either invest the money you deposit into your HSA or let it sit there.

Most people let the money sit there and lose value to inflation.

But just like a 401k or Roth IRA, you can use the HSA as an investment vehicle for low-cost index funds, gaining you an average 7% return on your money.

Here’s the kicker:

- In a 401k, you pay taxes when you withdraw the money.

- In a Roth IRA, you pay taxes when you put in the money.

This isn’t the case with an HSA.

In an HSA, you get triple tax savings whereas, in a 401k or Roth IRA, you only get double tax savings. You can read a comparison of these three types of accounts.

2. You Can Refund Medical Expenses Whenever You Want

You don’t have to pull any money out from your HSA when you have a medical expense.

You can still pay out-of-pocket.

If you save every single medical receipt you get while you have an HSA, you can refund those bills years and years down the line.

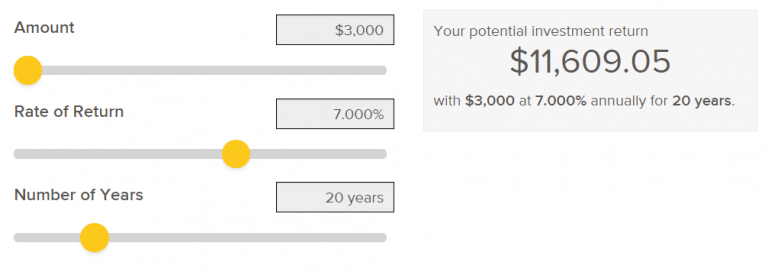

Take this example:

- I have an HSA invested with an average of

7%return - I invest

$3,000this year and invest nothing else (for simplicity) - I have a

$2,000medical bill

Option 1: Pay the $2,000 from my HSA right now

If I pay the $2,000 from my HSA right now, I would have $1,000 leftover in my HSA.

After 20 years, I would have ~$3,900 in my HSA.

Option 2: Pay the $2,000 out-of-pocket, save the receipt, and cash out $2,000 later

If I pay the $2,000 out-of-pocket, save the receipt, and cash out $2,000 in 20 years, my HSA would first grow to this:

Once I cash out, I would have $11,609.05 – $2,000 = $9,609.05 in my HSA, saving me roughly $5,700.

Now, this is only if I invest in my HSA for one year and never invest again. Imagine maxing out your HSA every year and deferring all your withdrawals until retirement. The savings would be massive.

3. You Can Pay Medical Expenses with a Credit Card

We’ve established that the money in your HSA should sit and grow over the course of your lifetime.

We can maximize our returns by paying these medical expenses out-of-pocket with a rewards credit card.

Depending on your card, you may get a 1%-3% cashback, which will just add to your overall returns.

4. You Can Wait Until You’re 65 Years Old

Once you turn 65, you HSA becomes a traditional IRA. That means you’re not restricted by medicals expenses.

This also means that you essentially have a 100% tax-free investment account at the age of 65 with no withdrawal restrictions. That’s just an investment paradise, isn’t it?

Remember, there is also no RMD, which means you can keep investing tax-free to your liking at your older age without taking out any money.

Steps to use HSA for retirement

- Pay all medical expenses out-of-pocket with a rewards credit card

- Digitally save medical receipts

- Regularly invest and allow investments to grow

- Wait until

65years of age for the HSA to function as an IRA - Cash out HSA with the medical receipts

- Use the HSA tax-free during retirement

Conclusion

HSAs are the secret to the F.I.R.E. (Financial Independence, Retire Early) movement.

Whether or not your goal is to retire early, these are things that anybody can use and take advantage of to save and invest as much money as you can